If the duration of a bond yielding 10% is 6 years, the volatility of the underlying interest rates 5% per annum, what is the 10-day VaR at 99% confidence of a bond position comprising just this bond with a value of $10m? Assume there are 250 days in a year.

Which of the following statements is NOT true in relation to the recent financial crisis of 2007-08?

The standard error of a Monte Carlo simulation is:

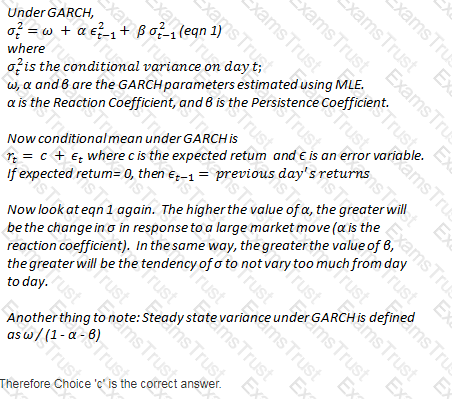

As the persistence parameter under GARCH is lowered, which of the following would be true:

Under the standardized approach to calculating operational risk capital, how many business lines are a bank's activities divided into per Basel II?

Which of the below are a way to classify risk governance structures:

A Reactive, Preventative and Active

B. Committee based, regulation based and board mandated

C. Top-down and Bottom-up

D. Active and Passive

When doing stress tests based on historical scenarios, if no appropriate historical scenarios exist for a security, it is most INAPPROPRIATE to:

What would be the consequences of a model of economic risk capital calculation that weighs all loans equally regardless of the credit rating of the counterparty?

I. Create an incentive to lend to the riskiest borrowers

II. Create an incentive to lend to the safest borrowers

III. Overstate economic capital requirements

IV. Understate economic capital requirements

For a given mean, which distribution would you prefer for frequency modeling where operational risk events are considered dependent, or in other words are seen as clustering together (as opposed to being independent)?

There are two bonds in a portfolio, each with a market value of $50m. The probability of default of the two bonds are 0.03 and 0.08 respectively, over a one year horizon. If the probability of the two bonds defaulting simultaneously is 1.4%, what is the default correlation between the two?

When building a operational loss distribution by combining a loss frequency distribution and a loss severity distribution, it is assumed that:

I. The severity of losses is conditional upon the number of loss events

II. The frequency of losses is independent from the severity of the losses

III. Both the frequency and severity of loss events are dependent upon the state of internal controls in the bank

Under the standardized approach to determining operational risk capital, operations risk capital is equal to:

Company A issues bonds with a face value of $100m, sold at $98. Bank B holds $10m in face of these bonds acquired at a price of $70. Company A then defaults, and the recovery rate is expected to be 30%. What is Bank B's loss?

If μ and σ are the expected rate of return and volatility of an asset whose prices are log-normally distributed, and Ψ a random drawing from a standard normal distribution, we can simulate the asset's returns using the expressions:

When pricing credit risk for an exposure, which of the following is a better measure than the others:

If an institution has $1000 in assets, and $800 in liabilities, what is the economic capital required to avoid insolvency at a 99% level of confidence? The VaR in respect of the assets at 99% confidence over a one year period is $100.

What does a middle office do for a trading desk?

Which of the following data sources are expected to influence operational risk capital under the AMA:

I. Internal Loss Data (ILD)

II. External Loss Data (ELD)

III. Scenario Data (SD)

IV. Business Environment and Internal Control Factors (BEICF)

If the default hazard rate for a company is 10%, and the spread on its bonds over the risk free rate is 800 bps, what is the expected recovery rate?

A risk analyst attempting to model the tail of a loss distribution using EVT divides the available dataset into blocks of data, and picks the maximum of each block as a data point to consider.

Which approach is the risk analyst using?

According to the Basel II standard, which of the following conditions must be satisfied before a bank can use 'mark-to-model' for securities in its trading book?

I. Marking-to-market is not possible

II. Market inputs for the model should be sourced in line with market prices

III. The model should have been created by the front office

IV. The model should be subject to periodic review to determine the accuracy of its performance

Which of the following statements are true:

I. The sum of unexpected losses for individual loans in a portfolio is equal to the total unexpected loss for the portfolio.

II. The sum of unexpected losses for individual loans in a portfolio is less than the total unexpected loss for the portfolio.

III. The sum of unexpected losses for individual loans in a portfolio is greater than the total unexpected loss for the portfolio.

IV. The unexpected loss for the portfolio is driven by the unexpected losses of the individual loans in the portfolio and the default correlation between these loans.

Which of the following describes rating transition matrices published by credit rating firms:

Which of the following cannot be used as an internal credit rating model to assess an individual borrower:

Which of the following statements is true in respect of a non financial manufacturing firm?

I. Market risk is not relevant to the manufacturing firm as it does not take proprietary positions

II. The firm faces market risks as an externality which it must bear and has no control over

III. Market risks can make a comparative assessment of profitability over time difficult

IV. Market risks for a manufacturing firm are not directionally biased and do not increase the overall risk of the firm as they net to zero over a long term time horizon

When performing portfolio stress tests using hypothetical scenarios, which of the following is not generally a challenge for the risk manager?

When modeling operational risk using separate distributions for loss frequency and loss severity, which of the following is true?

What percentage of average annual gross income is to be held as capital for operational risk under the basic indicator approach specified under Basel II?

For a US based investor, what is the 10-day value-at risk at the 95% confidence level of a long spot position of EUR 15m, where the volatility of the underlying exchange rate is 16% annually. The current spot rate for EUR is 1.5. (Assume 250 trading days in a year).

Which of the following distribution assumptions will produce the lowest probability of exceeding an extreme value, assuming identical means and variances?

Company A issues bonds with a face value of $100m, sold at issuance at $98. Bank B holds $10m in face of these bonds acquired at a price of $70. What is Bank B's exposure to the debt issued by Company A?

The cumulative probability of default for a security for 4 years is 11.47%. The marginal probability of default for the security for year 5 is 5% during year 5. What is the cumulative probability of default for the security for 5 years?

According to the Basel framework, reserves resulting from the upward revaluation of assets are considered a part of:

Which of the following statements is true in relation to the Supervisory Capital Assessment Program (SCAP):

I. The SCAP is an annual exercise conducted by the Treasury Department to determine the health of key financial institutions in the US economy

II. The SCAP was essentially a stress test where the stress scenarios were specified by the regulators

III. Capital buffers calculated under the SCAP represented the amount of capital that the institutions covered by SCAP held in excess of Basel II requirements

IV. The SCAP focused on both total Tier 1 capital as well as Tier 1 common capital

A stock that follows the Weiner process has its future price determined by:

If the full notional value of a debt portfolio is $100m, its expected value in a year is $85m, and the worst value of the portfolio in one year's time at 99% confidence level is $60m, then what is the credit VaR?

A portfolio's 1-day VaR at the 99% confidence level is $250m. What is the annual volatility of the portfolio? (assuming 250 days in the year)

If E denotes the expected value of a loan portfolio at the end on one year and U the value of the portfolio in the worst case scenario at the 99% confidence level, which of the following expressions correctly describes economic capital required in respect of credit risk?

The EWMA and GARCH approaches to volatility clustering can be applied to VaR calculations using:

If the annual variance for a portfolio is 0.0256, what is the daily volatility assuming there are 250 days in a year.

The daily VaR of an investor's commodity position is $10m. The annual VaR, assuming daily returns are independent, is ~$158m (using the square root of time rule). Which of the following statements are correct?

I. If daily returns are not independent and show mean-reversion, the actual annual VaR will be higher than $158m.

II. If daily returns are not independent and show mean-reversion, the actual annual VaR will be lower than $158m.

III. If daily returns are not independent and exhibit trending (autocorrelation), the actual annual VaR will be higher than $158m.

III. If daily returns are not independent and exhibit trending (autocorrelation), the actual annual VaR will be lower than $158m.

Which of the following is not an approach proposed by the Basel II framework to compute operational risk capital?

If the cumulative default probabilities of default for years 1 and 2 for a portfolio of credit risky assets is 5% and 15% respectively, what is the marginal probability of default in year 2 alone?

A bank's detailed portfolio data on positions held in a particular security across the bank does not agree with the aggregate total position for that security for the bank. What data quality attribute is missing in this situation?

Which of the following statements are true in relation to Monte Carlo based VaR calculations:

I. Monte Carlo VaR relies upon a full revalution of the portfolio for each simulation

II. Monte Carlo VaR relies upon the delta or delta-gamma approximation for valuation

III. Monte Carlo VaR can capture a wide range of distributional assumptions for asset returns

IV. Monte Carlo VaR is less compute intensive than Historical VaR

The degree distribution of the nodes of the financial network is:

An assumption regarding the absence of ratings momentum is referred to as:

Which of the following statements are true with respect to stress testing:

I. Stress testing results in a dollar estimate of losses

II. The results of stress testing can replace VaR as a measure of risk as they are better grounded in reality

III. Stress testing provides an estimate of losses at a desired level of confidence

IV. Stress testing based on factor shocks can allow modeling extreme events that have not occurred in the past

A corporate bond maturing in 1 year yields 8.5% per year, while a similar treasury bond yields 4%. What is the probability of default for the corporate bond assuming the recovery rate is zero?

An operational loss severity distribution is estimated using 4 data points from a scenario. The management institutes additional controls to reduce the severity of the loss if the risk is realized, and as a result the estimated losses from a 1-in-10-year losses are halved. The 1-in-100 loss estimate however remains the same. What would be the impact on the 99.9th percentile capital required for this risk as a result of the improvement in controls?

Which of the following credit risk models relies upon the analysis of credit rating migrations to assess credit risk?

Which of the following are measures of liquidity risk

I. Liquidity Coverage Ratio

II. Net Stable Funding Ratio

III. Book Value to Share Price

IV. Earnings Per Share

Which of the following is not an approach used for stress testing:

The diversification effect is responsible for: